In the UK, Corporation Tax is one of the most important things to think about when running a business. All limited companies have to pay it on their profits, and the rules are the same for small and large businesses. Companies don’t get any tax breaks, so they have to pay taxes on every pound of profit they make. This is different from personal income tax. If you know how Corporation Tax works, you can save money, plan ahead, and stay out of trouble with HMRC. We will explain everything in this blog so you can handle it with ease and focus on expanding your business.

What Is Corporation Tax

The main tax that limited companies in the UK pay on their profits is called Corporation Tax. It works like income tax, but instead of being charged to people, it is charged to businesses and some groups. If you are a sole trader, you pay income tax through Self Assessment. HMRC says that a limited company must pay Corporation Tax once it is set up.

The tax is worked out on the profit left after business expenses are taken away from income. This is before directors take a salary or dividends. Unlike personal tax there is no tax free allowance for companies. Corporation Tax is due from the very first pound of profit, which makes it one of the most important responsibilities for every limited company in the UK.

Who Needs to Pay Corporation Tax?

Corporation Tax must be paid by any limited company registered in the UK and this applies whether the company is trading, making a small profit or even no profit at all. A return still needs to be filed with HMRC to confirm the position. It is not limited to companies alone as clubs, co operatives, trade associations and certain charities also need to pay Corporation Tax if they earn profits from trading or activities outside their charitable work. In simple terms any organisation that makes profit is expected to pay Corporation Tax.

How Is Corporation Tax Calculated

Corporation Tax is worked out by taking the income a company earns from sales or services and then subtracting the business expenses that HMRC allows, such as staff wages, office costs, equipment and professional fees. The profit left after these deductions is called taxable profit and this is the figure used to calculate the tax owed. Not every expense can be claimed, so accurate records are important to avoid mistakes and penalties. If you want a quick way to check how much you might need to pay you can use our corporation tax calculator for an instant estimate.

Corporation Tax Rates in the UK

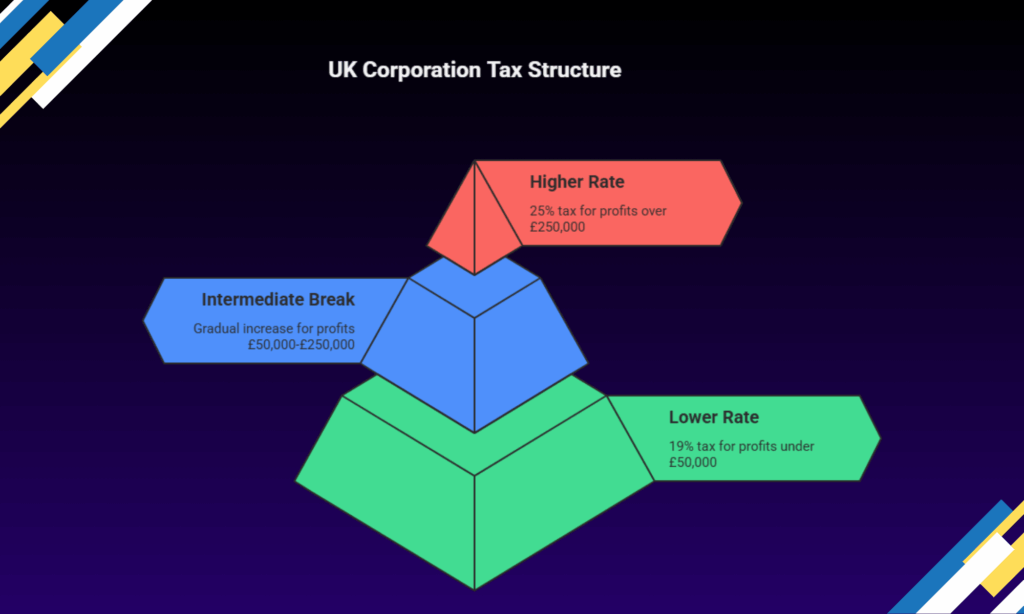

The UK charges different amounts of Corporation Tax depending on how much money a business makes. The system has been working in tiers since April 2023:

- Companies that make less than £50,000 pay 19% in taxes. Companies that make more than £250,000 pay 25%.

- Companies with profits between £50,000 and £250,000 get a small break, which means they don’t go straight to the higher rate.

This way, smaller businesses pay a lower rate, while bigger and more profitable businesses pay a higher rate. When making plans, it’s always a good idea to check the most recent HMRC advice because the rates can change with new government budgets.

When Do You Pay Corporation Tax

Corporation Tax is usually due nine months and one day after the end of your company’s accounting period. This means that the payment is often due before the Company Tax Return itself. A business with a year end of December 31 would have to pay by October 1 of the following year, but the return isn’t due until later. If you miss these dates, you could have to pay interest and fines, so it’s important to plan ahead. You can find all the important dates on our tax deadlines page to help you stay on track with your business.

Filing a Company Tax Return

The CT600, or Company Tax Return, is the form that a business must fill out to tell HMRC how much Corporation Tax it owes, as well as how much money it made and spent. It is done online and needs full accounts that follow accounting standards, which can be hard to understand if you have never done it before. Many businesses hire an accountant to help them feel better because mistakes can cost them time and money. You can make an appointment for a free consultation if you want professional help with filling out and filing your return. This way, you can be sure that everything is done right from the start.

Allowances and Reliefs You Should Know About

Paying money to HMRC is only one part of Corporation Tax. If your company meets certain requirements, there are a number of allowances and reliefs that can lower the final bill. Knowing how they work and turning in the right forms on time can really help your cash flow.

Annual Investment Allowance

A business can deduct the entire cost of its tools and equipment from its profits before corporation tax is computed thanks to the Annual Investment Allowance (AIA). This implies that you can purchase new equipment or technology and receive a refund during the same tax year. This helps you expand your business and save money.

Research and Development Relief

Research and Development Relief, or R&D Relief, is for companies that invest in improving their goods, services, or procedures. Developing a new system or enhancing an existing one can be advantageous for small businesses as well. The savings can be significant, but claims must be supported by thorough documentation and the appropriate HMRC forms. If the relief exceeds their tax bill, some businesses even receive cash credits.

Capital Allowances

Capital Allowances apply to big things like company cars, computer systems, or improvements to business property. Instead of treating these as normal costs, the cost is spread out over time, which lowers taxable profit each year. When making accounts, it’s important to use the right category because different rates apply to different types of assets.

Loss Relief

A business that loses money in trading doesn’t always waste money. You can use Loss Relief to carry the loss forward and use it to lower your Corporation Tax in later years. In some cases, it may be possible to get money back from HMRC for profits made in the past. You need to make the claim on the Company Tax Return and back it up with the right numbers.

Why Reliefs Matter

By using reliefs and allowances, you can lower your corporation tax bill by thousands of pounds. With the money they save, many businesses hire more employees, buy new equipment, or begin new projects. People usually miss out on these opportunities because they don’t know the rules or don’t fill out the necessary paperwork. Getting professional advice is essential because it guarantees that you can claim all of your rights and keep more money in the business.

How to File Corporate Taxes in 2025

To file corporate taxes in 2025, you must fill out the Company Tax Return online through HMRC and pay your Corporation Tax on time. Before submitting the CT600 form, a business must prepare comprehensive accounts that show all of its revenue and expenses and comply with accounting regulations. Generally, the payment is due nine months after the end of the accounting period, and the return is due within twelve months. If you keep your records organised throughout the year and get professional help, the process can go more smoothly and help you avoid fines.

Getting Help with Corporation Tax

Path Accountants helps UK businesses follow HMRC rules and lower their Corporation Tax bills by giving them the right advice and planning. We focus on giving clear instructions, keeping records of information correctly, and coming up with ways to cut costs while keeping the business running. We also offer a free consultation so you can talk about your needs before you make any decisions. You can make an appointment for your consultation and trust us to take care of everything.

The Future of Corporation Tax

The rules for Corporation Tax change a lot, and the changes that are planned for 2026 will change how many businesses pay their bills. Getting ready early helps businesses stay ahead and not be surprised.

Changes will happen in 2026 Corporation Taxes

- Limits on how much credit loss-making, R&D-heavy small and medium-sized businesses can get

- Changes to capital allowances as temporary tax breaks go away

- A look at marginal relief for companies with a medium size

- Progress on digital reporting for corporation tax under Making Tax Digital

Businesses can stay compliant and protect their profits by keeping up with these changes and reviewing their tax planning every year.

Final Thoughts

You have to pay corporation tax if you own a business in the UK. Management is easier when you have well-organised records, know the rules, and use the right reliefs. If you think of it as a normal business need instead of a burden, it will keep your business legal and strong. You can grow your business without worrying about tax problems that come up out of the blue if you plan ahead and get the right help.

FAQs

What is the current rate of Corporation Tax in the UK?

The main rate of Corporation Tax is 25% for companies with profits above £250,000. Smaller companies with profits up to £50,000 pay 19% and those in between can claim marginal relief.

When does a company need to pay Corporation Tax?

Corporation Tax is normally due nine months and one day after the end of the company accounting period. The Company Tax Return is due later, within twelve months of the year end.

Can small businesses reduce their Corporation Tax bill?

Small businesses can save money on their taxes by taking advantage of things like the Annual Investment Allowance, Research and Development Relief, and Capital Allowances. Keeping good records and filing on time also helps you avoid fines that make things more expensive.

What happens if a company does not pay Corporation Tax on time?

If a company doesn’t pay on time, HMRC will charge interest and may even add fees. It is always better to plan ahead and pay early because the business will have to pay more the longer the delay.

Do companies have a tax free allowance for Corporation Tax?

Companies do not get a tax free allowance in the way individuals do with income tax. Corporation Tax is charged from the very first pound of profit made by the company.

Get expert help before your next tax deadline.

Path Accountants helps UK small businesses stay compliant, organised, and tax efficient.

Mohammad Hamza Pathan

ACA Chartered Accountant & Technical Reviewer

ICAEW verified practising certificateMohammad Hamza Pathan is an ICAEW Chartered Accountant and a director of Path Accountants. He reviews Path Accountants guides for technical accuracy, practical relevance and alignment with current UK accounting and tax requirements before publication or substantive updates.

Qualifications and experience

- ICAEW Chartered Accountant (ACA), admitted in 2020 and holder of an ICAEW practising certificate.

- Accountant at Path Accountants and a registered director of Path Accountants Ltd.

- Education listed as Cass Business School.

Professional review areas

- UK tax compliance

- Statutory and company accounts

- Self Assessment

- VAT and Making Tax Digital

- Bookkeeping and payroll

- Small-business accounting

Technical claims, UK terminology, key compliance points and whether the guidance clearly distinguishes general information from advice that depends on a reader's circumstances.